During the summer of 2020, as the COVID-19 pandemic caused market fluctuations, SoftBank Group stunned Wall Street by executing a series of large options trades on U.S. tech stocks. Leading these transactions—earning SoftBank the nickname “Nasdaq whale”—was Akshay Naheta, an executive renowned for taking calculated risks in the face of disruption.

Having facilitated multi-billion-dollar deals, including a proposal to merge Nvidia with ARM, Naheta is now embarking on what could be his most daring venture yet: reimagining the global payment infrastructure.

His startup, Distributed Technologies Research (DTR), based in Zug, Switzerland, aims to close the divide between conventional banking and blockchain technology, joining a multitude of companies seeking to enhance global payment systems.

DTR asserts that its technology can address numerous payment inefficiencies, including transfer fees, interchange charges, foreign exchange conversion rates, and delays in settlement. “Existing payment networks are hampered by various inefficiencies—transfer fees, interchange rates, FX conversion costs, settlement delays, and other non-transparent charges,” Naheta explained in a conversation with TechCrunch.

At the heart of DTR’s technology is AmalgamOS, which acts as a bridge between banks and blockchain networks. By utilizing APIs, it allows businesses to embed payment functions while remaining compliant with regional regulations. The system is designed to support diverse transactions ranging from merchant payments to treasury management and accommodates both traditional currencies and major stablecoins across 48 nations.

DTR boasts what Naheta refers to as an “international orchestration network” that intelligently directs transactions through either traditional banking or blockchain pathways, depending on the most efficient balance of speed and cost. “We are connected to 12,000 banks in Europe,” he stated in an interview, emphasizing that businesses that integrate DTR’s APIs can enable their customers to initiate transfers directly via banking applications.

DTR’s venture into payment infrastructure is timely, coinciding with growing scrutiny over Visa and Mastercard—both of which impose swipe fees of 2% to 3%, typically among the highest expenses for merchants following payroll. The proposed Credit Card Competition Act in the U.S. could mandate that banks provide merchants with alternatives to these dominant networks.

Early adopters of DTR’s infrastructure have reported significant benefits. For instance, Phillip Lord of Oobit, a cryptocurrency wallet startup, noted that the system enabled his firm to transfer money from a crypto wallet to a U.K. bank account on Christmas Day in under 30 seconds—a process that would normally take days through traditional methods.

Image Credits:DTR

Naheta’s focus on payment infrastructure can be traced back to an unexpected incident: SoftBank’s acquisition of Fortress Investment Group in 2017, which positioned Bitcoin worth approximately $20 million on SoftBank’s balance sheet.

Intrigued by blockchain technology, Naheta recognized potential applications for his expertise in wireless communications within payment networks. While still at SoftBank, he began gathering what would become the DTR founding team. He reached out to his undergraduate thesis advisor, Pramod Viswanath, renowned for his wireless communications knowledge, who now heads Princeton’s blockchain center, and Sreeram Kannan, who eventually co-founded EigenLayer.

The team viewed blockchain as a decentralized communications platform that could leverage years of research in wireless technologies to innovate payments. Naheta considered resigning from SoftBank in summer 2018 to devote himself to DTR and the crypto venture Bakkt but ultimately decided to remain, encouraged by senior executives like Rajeev Misra and Masayoshi Son.

Naheta’s past efforts in the payments space included SoftBank’s investment in the now-defunct Wirecard; nonetheless, they still profited from their involvement. “I’ve encountered plenty of missteps,” he admitted. “I evaluated it from the standpoint of a company equipped with regulated licenses worldwide, clearly possessing payment technology.”

These experiences seem to have shaped DTR’s focus on compliance and institutional integrity, a cautious strategy that extends to the company’s growth plans. “Even if I increase my team to 60 members by the next quarter, we will still be free cash-flow positive,” he stated.

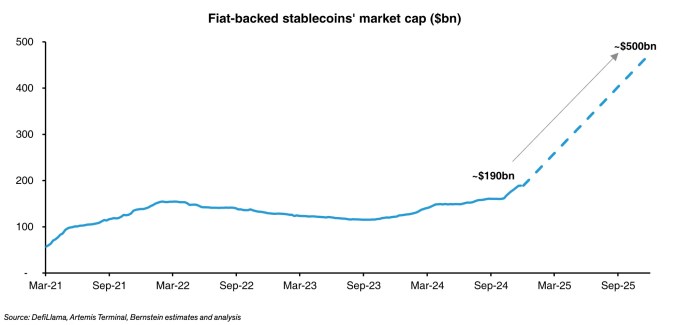

Image Credits:Bernstein

DTR is contending with competition from various sources. Wise has successfully matched currency flows across borders, Ripple provides blockchain-based settlements despite ongoing legal challenges, and traditional banks are revitalizing their systems via projects like SWIFT. Additionally, Stripe’s recent $1 billion acquisition of Bridge is expected to deepen its engagement in the payments sector.

Nonetheless, Naheta believes there is a niche to serve businesses caught amid these transformations—particularly those involving digital nomads, creator economy platforms, and enterprises working across emerging markets.

“Banks are ill-equipped to manage KYC/AML regulations at such a granular level, especially when facilitating payouts of $200 to 10,000 individuals monthly,” he contends. The fragmented nature of national payment frameworks presents challenges for global businesses, as each jurisdiction has distinct systems and regulations.

The payment sector’s impressive profit margins and network effects make it notoriously challenging to disrupt. PayPal boasts a market cap nearing $70 billion even amid recent downturns, and Visa and Mastercard collectively are valued at over $1 trillion.

“I genuinely believe that retail customers are being shortchanged in the payment arena,” he posits. “It’s not solely the banks’ fault; they are entrenched in legacy systems, making it exceptionally difficult to turn a Titanic.”

Lord from Oobit remarked in a discussion that the landscape remains largely unexplored. He highlighted that until a year ago, businesses needing to transition between crypto and conventional banking had to resort to “OTC shops and pay 1% to 3% to facilitate the transfer.”

“It’s astonishing that for so long, despite numerous startups and coin developments, there was no established legal framework for seamless on-ramping or off-ramping,” he noted. DTR’s solution aims to be “a block faster” than the alternatives currently available.

Compiled by Techarena.au.

Fanpage: TechArena.au

Watch more about AI – Artificial Intelligence